Chicago school of economics

Videos

Photos

The Chicago school of economics is a neoclassical school of economic thought associated with the work of the faculty at the University of Chicago, some of whom have constructed and popularized its principles. Milton Friedman, and George Stigler are considered the leading scholars of the Chicago school.

Department of Economics at the University of Chicago

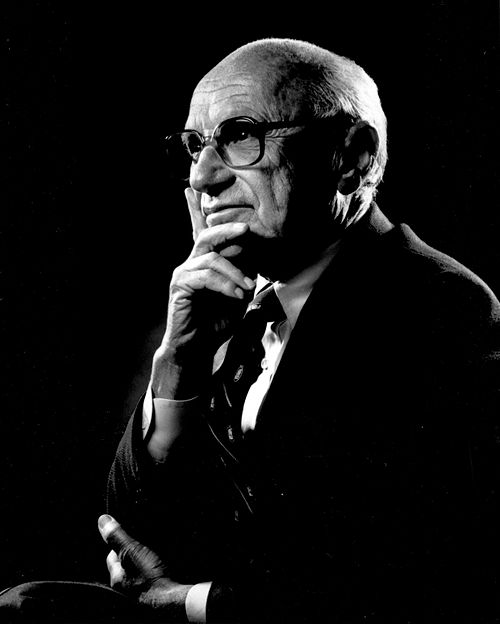

The Nobel laureate Milton Friedman was affiliated with the University of Chicago for three decades; his ideas and his students made significant contributions to the development of Chicago School theory.

Gary Becker (May 24, 2008)

Nobel laureate Gene Fama is often called the "father of modern finance" for his contributions to the study of finance.

University of Chicago

Videos

Photos

The University of Chicago is a private research university in Chicago, Illinois. The university has its main campus in Chicago's Hyde Park neighborhood.

Albert A. Michelson, Professor of Physics and first American Nobel laureate, delivers the second Convocation Address in front of Goodspeed and Gates-Blake Halls, with President William Rainey Harper, professors, and trustees in attendance, July 1, 1894.

View from the Midway Plaisance

The campus of the University of Chicago, from the top of Rockefeller Chapel, the Main Quadrangles can be seen on the left (West), the Institute for the Study of Ancient Cultures, West Asia & North Africa and the Becker Friedman Institute for Research in Economics can be seen in the center (North) and the Booth School of Business and Laboratory Schools can be seen on the right (East), as the panoramic is bounded on both sides by the Midway Plaisance (South).

View of university building from the Harper Quadrangle