In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor. The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

1978 $1,000 U.S. Treasury bond

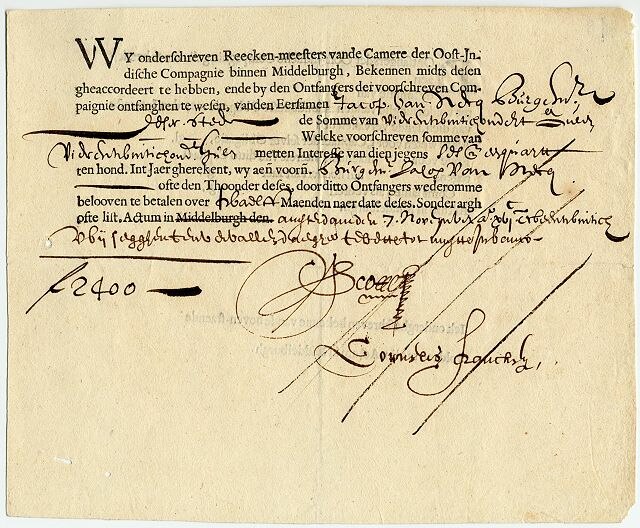

Bond issued by the Dutch East India Company in 1623

Bond certificate for the state of South Carolina issued in 1873 under the state's Consolidation Act

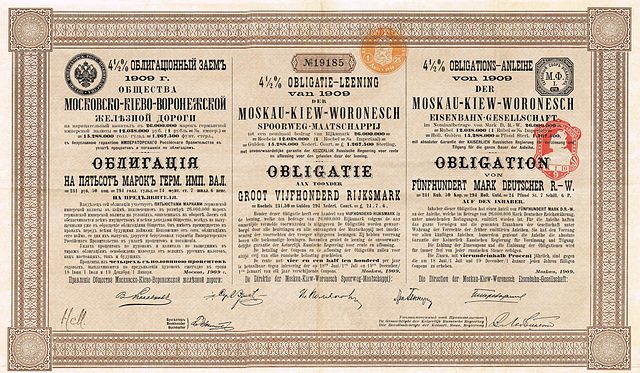

Railroad obligation of the Moscow-Kiev-Voronezh railroad company, printed in Russian, Dutch and German

Finance is the study and discipline of money, currency and capital assets.

It is related to but distinct from economics, which is the study of the production, distribution, and consumption of goods and services.

Based on the scope of financial activities in financial systems, the discipline can be divided into personal, corporate, and public finance.

Bond issued by The Baltimore and Ohio Railroad. Bonds are a form of borrowing used by corporations to finance their operations.

Share certificate dated 1913 issued by the Radium Hill Company

NYSE's stock exchange traders floor c 1960, before the introduction of electronic readouts and computer screens

Chicago Board of Trade Corn Futures market, 1993