Eugene Fama

Videos

Page

Eugene Francis "Gene" Fama is an American economist, best known for his empirical work on portfolio theory, asset pricing, and the efficient-market hypothesis.

Fama in Stockholm, December 2013

Modern portfolio theory

Videos

Page

Modern portfolio theory (MPT), or mean-variance analysis, is a mathematical framework for assembling a portfolio of assets such that the expected return is maximized for a given level of risk. It is a formalization and extension of diversification in investing, the idea that owning different kinds of financial assets is less risky than owning only one type. Its key insight is that an asset's risk and return should not be assessed by itself, but by how it contributes to a portfolio's overall risk and return. The variance of return is used as a measure of risk, because it is tractable when assets are combined into portfolios. Often, the historical variance and covariance of returns is used as a proxy for the forward-looking versions of these quantities, but other, more sophisticated methods are available.

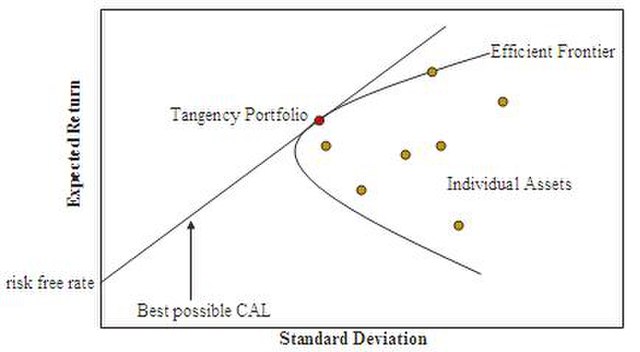

Efficient Frontier. The hyperbola is sometimes referred to as the 'Markowitz Bullet', and is the efficient frontier if no risk-free asset is available. With a risk-free asset, the straight line is the efficient frontier.