Federal Reserve Act

Videos

Photos

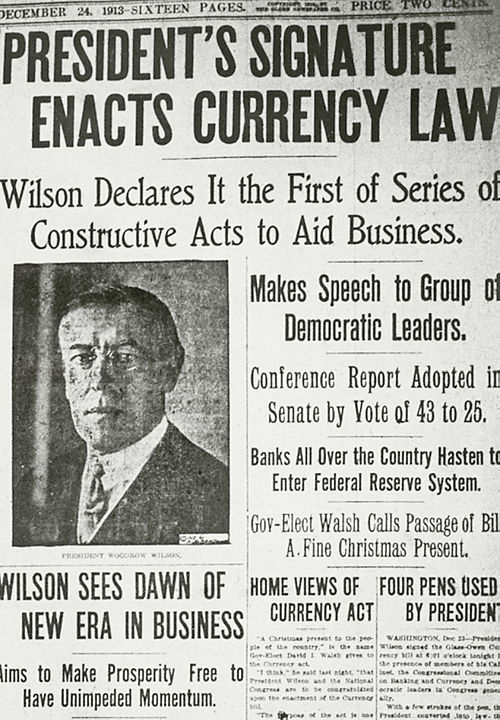

The Federal Reserve Act was passed by the 63rd United States Congress and signed into law by President Woodrow Wilson on December 23, 1913. The law created the Federal Reserve System, the central banking system of the United States.

Federal Reserve

63rd United States Congress

Videos

Photos

The 63rd United States Congress was a meeting of the legislative branch of the United States federal government, composed of the United States Senate and the United States House of Representatives. It met in Washington, D.C. from March 4, 1913, to March 4, 1915, during the first two years of Woodrow Wilson's presidency. The apportionment of seats in the House of Representatives was based on the 1910 United States census.

United States Capitol (1906)

Inauguration platform being constructed on the east steps of the U.S. Capitol, ten days before Woodrow Wilson's March 4, 1913, presidential inauguration.

Thomas R. Marshall (D)

Champ Clark (D)