Supply-side economics is a macroeconomic theory postulating that economic growth can be most effectively fostered by lowering taxes, decreasing regulation, and allowing free trade. According to supply-side economics, consumers will benefit from greater supplies of goods and services at lower prices, and employment will increase. Supply-side fiscal policies are designed to increase aggregate supply, as opposed to aggregate demand, thereby expanding output and employment while lowering prices. Such policies are of several general varieties:Investments in human capital, such as education, healthcare, and encouraging the transfer of technologies and business processes, to improve productivity. Encouraging globalized free trade via containerization is a major recent example.

Tax reduction, to provide incentives to work, invest and take risks. Lowering income tax rates and eliminating or lowering tariffs are examples of such policies.

Investments in new capital equipment and research and development (R&D), to further improve productivity. Allowing businesses to depreciate capital equipment more rapidly gives them an immediate financial incentive to invest in such equipment.

Reduction in government regulations, to encourage business formation and expansion.

Robert Mundell popularized the theory of supply-side economics after developing the theory with Arthur Laffer in the 1970s

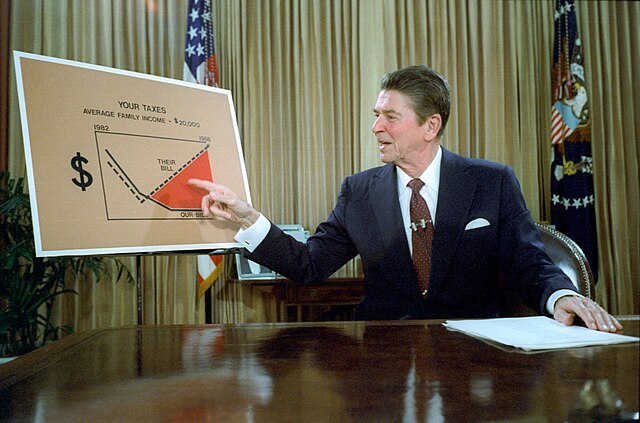

Ronald Reagan gives a televised address from the Oval Office, outlining his plan for tax reductions in July 1981

Supply side economics has been criticised for benefiting high income earners, as graph shows the change in top 1% income share against the change in top income tax rate from 1975–1979 to 2004–2008 for 18 OECD countries: the correlation between increasing income inequality and decreasing top tax rates is very strong

In economics, the Laffer curve illustrates a theoretical relationship between rates of taxation and the resulting levels of the government's tax revenue. The Laffer curve assumes that no tax revenue is raised at the extreme tax rates of 0% and 100%, meaning that there is a tax rate between 0% and 100% that maximizes government tax revenue.

Arthur Laffer

Figure compares the Laffer curve under the assumption that firms do not respond to changes in the tax rate (Naïve) to the Laffer curve when firms adjust their prices (Firm Response) as estimated in Miravete, Seim, & Thurk (2018). The tax revenue-maximizing rates are indicated in parentheses.