Management accounting

Videos

In management accounting or managerial accounting, managers use accounting information in decision-making and to assist in the management and performance of their control functions.

IFAC Definition of enterprise financial management concerning three broad areas: cost accounting; performance evaluation and analysis; planning and decision support. Managerial accounting is associated with higher value, more predictive information. Copyright July 2009, International Federation of Accountants

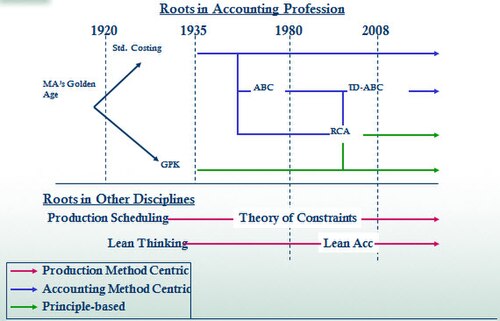

Managerial costing time line Used with permission by the author A. van der Merwe. Copyright 2011. All Rights Reserved.

Founded in 1904, the Association of Chartered Certified Accountants (ACCA) is the global professional accounting body offering the Chartered Certified Accountant qualification (ACCA). It has 240,952 members and 541,930 future members worldwide. ACCA's headquarters are in London with principal administrative office in Glasgow. ACCA works through a network of over 110 offices and centres in 51 countries - with 346 Approved Learning Partners (ALP) and more than 7,600 Approved Employers worldwide, who provide employee development.

ACCA advertisement on a Hong Kong tram

The art deco Adelphi building from the 1930s, located at 1-10 John Adam Street in London, is the current HQ of ACCA